We all know medical bills can be expensive. You've probably been hit with mild shock at least once when looking at the total amount due.

Thankfully, plenty of viable options exist to lower the bill or erase it entirely. Reducing your medical bills is easier than you think!

Here's how to do it, step by step.

1. Request an Itemized Bill

Imagine getting your receipt at Trader Joe’s and it just says: “FOOD – $89.23” on it. Or you drop your car at the mechanic, and when you pick it up, they give you a bill that reads “WE FIXED YOUR CAR – $1,619.79.”

In both cases, you’d probably want something much more specific. That should always be your first reaction to your medical bill, too.

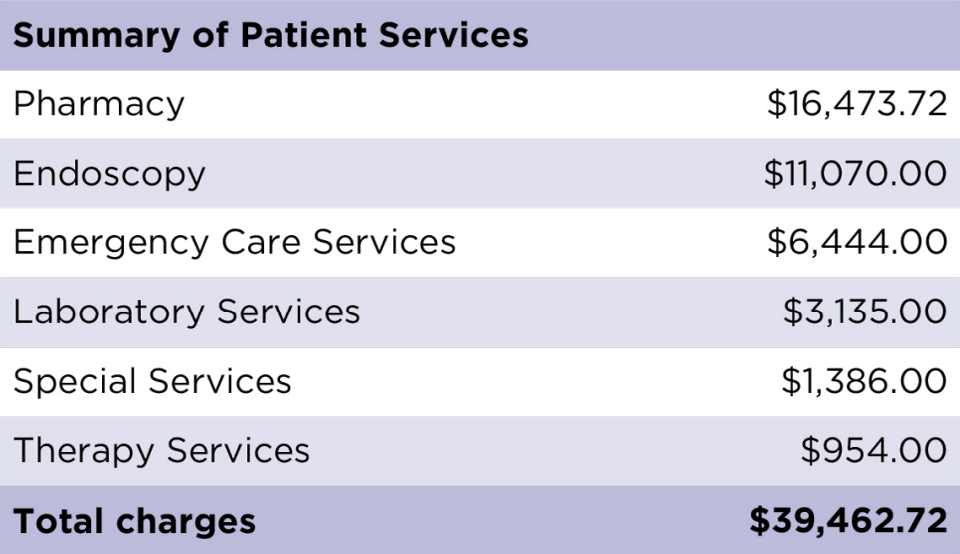

Because, for some reason, it’s common practice for medical billing departments to bucket individual charges together into “summary charges” like “Pharmacy” and “Special Services.”

Source: Sharp HealthCare

Summary of charges

These vague and unhelpful “summary charges” may save on paper, but they also make it impossible to see what you’re really being billed for — and whether you’re being charged for something by mistake.

And statistically speaking, you probably are. A 2011 study by the Access Project found that up to 80% of medical bills have errors on them — things like duplicate charges, incorrect billing codes, or patients being charged for services and procedures they never even received.

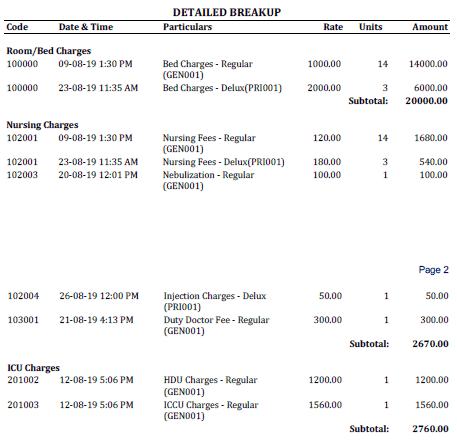

Call the hospital billing department and ask for an itemized bill with billing codes attached. You should then receive something way more detailed and helpful like this:

Source: MyOPD

Granted, much of a medical bill will still read like gibberish to anyone without a medical background. But you don’t need an MD to scan for errors like duplicate codes, bed charges for days you weren’t even a patient, and other obvious mistakes that can take thousands off your medical costs.

You should also know that seeing your own billing information is a federally protected right under HIPAA law 45 CFR § 164.524.

Despite this, a 2023 study by Goodbill found that nearly 60% of hospitals didn’t honor patients’ requests to see their own billing information. So you may have to be persistent and politely (but firmly) remind the billing department of your rights.

2. Request an Explanation of Benefits (EOB) From Your Insurance

If you have health insurance, your next step is to check that your insurance company got it right, too.

In a typical billing situation, healthcare providers will bill your insurance company first. Your insurance company will then cover some or all of the charges and send the rest back to your provider, who then sends the leftover balance to you.

In the end, you’ll get a bill showing:

- Your charges

- What your insurance covered

- What’s left for you to cover

Your job is to make sure your insurance company covers everything they were supposed to cover — in the right amounts.

Explanation of benefits

You’ll need to have both your itemized bill and your insurance plan’s explanation of benefits (EOB). The latter summarizes everything your health insurance plan does and doesn’t cover, including things like copays, deductibles, and more.

Insurance providers typically send paper copies of your EOB after sign-up. But if you’ve lost it, you can request another or possibly find a digital version in your online account.

Just this year, I’ve found two errors doing this. In one case, my provider charged for a Level 5 visit while my insurance paid for a Level 4 visit, leaving me with a much bigger medical bill by mistake.

In another instance, my provider didn’t apply one $500 physical therapy visit to my annual deductible, so my next bill was erroneously $500 higher.

Even if you don’t find any errors, a simple refresher of your policy can provide peace of mind and perhaps point out benefits you forgot to use, like discounted gym memberships.

RELATED: How to Use Your HSA to Unlock Preventative Care Savings

3. Ask the Hospital for Their Financial Assistance Policy

As part of a lesser-known clause in the Affordable Care Act, all hospitals with 501(c)(3) status are required to provide free or discounted care to qualifying patients, also known as “charity care.” Many for-profit hospitals offer financial assistance programs as well.

In either case, you can often find your provider’s written Financial Assistance Policy (FAP) by simply Googling or asking the billing team.

To qualify for financial assistance with a non-profit hospital, you need to be uninsured and make below 400% of the current year’s national poverty level.

For-profit hospitals may have a lower threshold (which, to be clear, excludes more patients). Kaiser Permanente, for example, set theirs at 300%.

If you think you may qualify for assistance with hospital bills, it’s certainly worth having another transparent conversation with billing and filling out an application if you're eligible.

4. Ask for a Reduced Fee

Even if you don’t qualify for financial assistance, some hospitals may still lower medical bills. That is, if you can demonstrate that the outstanding balance would cause you financial hardship.

For example, you might make $60,000 — which is right outside the boundary for financial assistance — but your rent and student loans already gobble up most of your paycheck.

To find out if you might qualify for this “hidden” financial assistance, simply ask billing on the phone whether they might offer a “reduced fee for financial hardship.”

Be sure to mention that you have the tax returns, pay stubs, and lease agreements to back up your claims.

They may not, but it’s certainly worth the ask.

5. See if You Qualify for Medicaid

Qualifying for Medicaid could seriously slash your current and future medical bills.

For the uninitiated, Medicare and Medicaid are different. Medicare is federally subsidized health insurance for folks aged 65 and over.

Medicaid, on the other hand, is for folks with disabilities. Depending on the state, you may qualify for Medicaid if:

- You think you are pregnant

- You’re a child or teenager

- You’re in foster care

- You’re legally blind

- You have a disability

- You need nursing home care

- You and your family are on Supplemental Security Income (SSI) or are low-income in general

To find out more details, visit your state’s official Medicaid page. Since there’s a boatload of Medicare/Medicaid-related scams out there, be sure that any application you fill out comes directly from a trustworthy source, ideally ending in .gov, such as medicaid.georgia.gov.

RELATED: What Is Disability Insurance and Is It Worth Buying?

6. Hop on a Payment Plan

Most medical billing departments won’t expect you to pay giant medical bills in full right away. In fact, bills of all sizes often come with payment plan options listed right on the bill itself. And in many cases, you can even pay off your debt interest-free.

That’s a really big deal because it means you don’t have to take out a high-interest personal loan or use your credit card for medical costs. Both of which could lead you spiraling into debt.

Instead, if the hospital offers a 0% interest payment plan, take it. You’ll get extra time to pay off your hospital bills without interest accruing.

7. Next Time, Ask for a “Good Faith Estimate”

Have you ever been told that “we don’t provide pricing upfront,” only to be blindsided by a huge medical bill later?

There’s a way to prevent that from ever happening again. Better still, uttering the magic words before your visit may even save you thousands of dollars when your bill arrives.

Those magic words are: “Could you please provide me with a good faith estimate?”

While it may sound like the medical equivalent of a wink and a “how ‘bout a good guy discount?“, Good Faith Estimates are actually a federally protected right.

Thanks to the No Surprises Act, a patient who requests a Good Faith Estimate before receiving medical care is entitled to a sincere, best-guess estimate of how much their visit will cost.

Then, if you get the bill and it’s more than $400 higher than your Good Faith Estimate, you can dispute it through the patient-provider dispute resolution process.

But providers don’t like being reported to the Feds, so you may see faster results by simply calling billing, sending them a copy of your Good Faith Estimate, and asking for a price adjustment.

FAQs

Can I negotiate medical bills even if I have insurance?

Absolutely. Even with insurance, you can still dispute billing errors, ask about financial hardship programs, or request payment plans for your remaining balance.

Will negotiating my medical bills hurt my credit score?

No, negotiating payment plans or asking for billing corrections won't impact your credit. However, if you ignore bills entirely and they go to collections, that's when your credit score could take a hit. Always communicate with billing departments to avoid this.

Should I pay anything while I'm disputing errors or negotiating?

If you can, pay what you know is correct to show good faith, but don't pay disputed charges until they're resolved. For example, if your bill is $3,000 but you found a $500 duplicate charge, pay $2,500 and note that you're disputing the rest. This shows the hospital you're serious about paying what you actually owe.

TL;DR: Negotiating Medical Bills

You have more power to reduce your medical bills than you might think.

Ask for an itemized bill and get your insurance's explanation of benefits to catch any billing errors.

If you can't afford to pay, look into financial assistance programs that many hospitals are legally required to offer. Even if you don't qualify for charity care, you can still negotiate reduced fees based on financial hardship.

Before any medical procedure, ask for a “Good Faith Estimate” — it's your federally protected right and gives you leverage if the final bill is $400+ higher.

Remember: Hospitals would rather work with you than send bills to collections, so don't be afraid to advocate for yourself!

Learn With Erika

- Free Travel Secrets Workshop

- Learn how to use the fine print to book your next vacation practically for free with Erika's step-by-step system

- Free 5 Day Investing Challenge

- Learn how to get started as a beginner investor and make your first $10,000

- Free 5 Day Savings Challenge

- Discover how you can save $1,000 without penny pinching or making major life sacrifices

- Join Erika Kullberg Insiders

- Ask investing questions, share successes and participate in monthly challenges and expert workshops