“The best time to plant a tree was 20 years ago; the second-best time is today.”

While that saying has been misattributed to everyone from Confucius, to Solomon, to Abraham Lincoln, the root meaning is no less true. Something worth doing 20 years ago is still worth doing today.

You’ve probably read news articles stating that today’s 50-year-olds are dreadfully unprepared for retirement. Those headlines are often filled with fatalistic language like, “Work until you die.”

I’d like us to dispense with all that. While it’s true that saving for retirement is a numbers game and longer time horizons are easier to prepare for than short ones, it’s not impossible to save for a good retirement even if you start at 50.

Just like the proverbial tree, the best time to start saving for retirement was with your first paycheck — but the second-best time is with your next paycheck.

Financial Planning in Your 50s

At the heart of your financial plan are numbers. And there are several important industry benchmarks to consider.

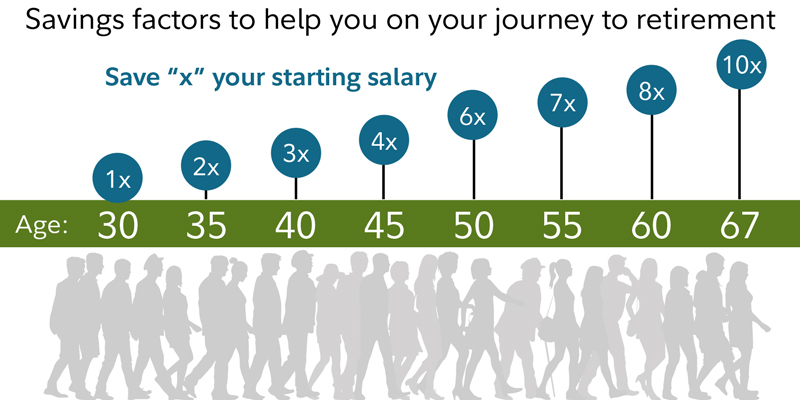

Fidelity Investments has long published the guideline that you should have 6x your salary saved by age 50 to put you on track for retirement by age 67.

According to data from the U.S. Bureau of Labor and Statistics, the median annual salary for those aged 45-54 was $69,472 as of the last quarter of 2024.

So, by the Fidelity benchmark, you’d need to have saved $416,832 to be on track for retirement by your 50th birthday.

But if you don’t have that, you’re not alone.

Vanguard’s annual study of its 401(k) participants found that, in 2023, the average 401(k) balance was $142,069 for folks aged 45-54.

But there are a couple of caveats to that. The first is that statistical outliers (i.e., folks with huge balances) drive the average up. Because of that, a more useful figure is the median. For 2023, that median balance was just $48,301.

The second caveat is that Vanguard’s study only included people with an account at Vanguard. Since one in four Americans has no retirement account at all, the median for all households would drop substantially if they were included.

READ MORE: How Much You Need to Retire

How To Invest for Retirement at Age 50

Saving and investing for retirement is simple — but not necessarily easy.

The steps are well-known: live on less than you make, control your lifestyle, save the difference, and invest that in a well-diversified portfolio with age-appropriate risk.

What might surprise you is that, in some ways, saving as a 50-year-old is easier than in your 20s or 30s.

Here are some steps you can take today.

Get your cash right

Americans in general tend to have too little in liquid savings — i.e., an emergency fund.

Having an emergency fund gives stability to your investments since you won’t need to raid your 401(k) or IRA every time life gives you lemons.

Most finance experts suggest something between three and six months of expenses — but several recommend six months or more for folks in their 50s.

READ MORE: How Much Can I Afford to Invest?

Don’t leave free money on the table

According to research by the investment firm Financial Engines, Americans leave more than $24 billion in unclaimed 401(k) employer matches on the table each year.

By examining 4.4 million participants at 553 companies, they found that 25% of workers fail to claim the full employer match.

If your employer offers a 401(k) match, tap into that free money immediately.

Invest in boring but stable assets

At this stage of life, you will most likely want a diversified portfolio made up of stocks, bonds, and cash. At 50, you’re on the cusp of reducing your risk tolerance, since your time horizon to retirement is shorter.

Swinging for the fences at 25 is a much different proposition than when you’re in your 50s and have just a few years to get it right. Attempting to make up lost time by taking on more risk is a fool’s errand.

It’s time to start thinking in terms of stability: boring stuff like major indexes, balanced funds, and mutual funds instead of the latest fads.

All major brokerages offer low-cost target date index funds correlated to your retirement date. They are the epitome of simplicity for new investors — pick your retirement date, pick your contribution amount, and let it go to work while you go live your life.

Such target date index funds are the default investment in most 401(k)s and 403(b)s and are widely available across retirement plans.

READ MORE: Long-Term vs. Short-Term Investment Strategies

Take advantage of your wage

Salaries tend to increase steadily before peaking in your 40s, and then remain elevated through your 60s. And for most people, your 50s are a time when your children are likely grown and perhaps you’ve paid down your mortgage. You’re typically more settled in your life and career.

All of this means that your disposable income should be higher in your 50s and 60s than at any other time in your life.

According to the Bureau of Labor and Statistics, the average 50-year-old makes 20% more than the average 30-year-old. If you’ve undersaved for retirement, leverage that income to boost your savings rate.

Let the government help

At age 50, workers become eligible for “catch-up contributions,” and your limits for 401(k) and IRA contributions get a bump.

The limit for 401(k) contributions in 2026 is $24,500, but if you’re 50 or older, that limit increases by $8,000, or if you're aged 60 to 63, it increases by $11,250

IRA contributions are limited to $7,500, but if you’re 50 or older, you can save up to $8,600

The government knows you're trying to catch up and has increased the limits on tax-advantaged accounts to help.

Put on your own oxygen mask first

Finally, beware of lingering financial care for adult children and ongoing college expenses. Yes, you may want to help your kids into adulthood, but if you haven’t sorted out your own retirement, it’s an expense you can’t afford.

Your kids can fund a first house or tuition in several ways, but you have one way to fund your retirement: you.

FAQs

What is the best investment for a 50-year-old?

Aim for a diversified portfolio made up of stocks, bonds, and cash. In your 50s, you should be leaving high-risk and speculative investments in the rear-view mirror, particularly if you’ve undersaved to this point.

Target date index funds are the default investment in most 401(k)s and 403(b)s and are widely available across retirement plans. For folks new to investing and nervous about markets, they present the simplest solution to get started.

At what age should you stop investing?

The short answer is never.

The longer answer is that investing and saving are two very different things despite often being used interchangeably.

Saving is putting away money you plan to spend. You may earn a little interest on those funds, but you are largely spending the dollars you put in.

Investing has a much longer time horizon and the goal is to generate gains in the form of appreciation, dividends, and interest that you can spend while leaving the investment itself intact.

Saving is like buying apples to put in your pantry to eat next week. Investing is like buying an orchard to eat apples out of 20 years from now. Since we all will need some form of income right up until the end of our life, there’s no logical reason to stop investing before that.

The Bottom Line

Starting to save at 50 is a daunting task, but take heart — if you can steadily save until your full retirement age, you can still retire well.

A late start will make early retirement unlikely and you’re pretty much out of the FIRE (“financial independence, retire early”) movement by default, but a retirement of “enough” is still in reach.

Starting this week is better than not starting at all.

For more investing insights at any age, check out these episodes of the Erika Taught Me podcast:

- The Missing Piece in 99% of Financial Advice

- Money & Investing Pitfalls to Avoid

- The Psychology of Money

Learn With Erika

- Free Travel Secrets Workshop

- Learn how to use the fine print to book your next vacation practically for free with Erika's step-by-step system

- Free 5 Day Investing Challenge

- Learn how to get started as a beginner investor and make your first $10,000

- Free 5 Day Savings Challenge

- Discover how you can save $1,000 without penny pinching or making major life sacrifices

- Join Erika Kullberg Insiders

- Ask investing questions, share successes and participate in monthly challenges and expert workshops

. . .